Economic Commentary – Review of Q4/2023

The economy

Globally, economic growth for 2023 was 2.9%, down from the 3.5% growth experienced in 2022. Interest rates around the world were maintained at elevated levels to combat high inflation that followed the very loose monetary policy after the Covid pandemic of 2020.

In the United States (US), the Federal Reserve Bank increased the federal funds rate to 5.5%. US government bond yields strengthened during the first quarter of 2023 but weakened substantially by the end of the third quarter. The benchmark US 10-year government bond yield traded as high as 4.99% but closed the year at 3.87%.

Inflation came down in 2023 but has not reached the target levels maintained by monetary authorities in several countries around the world. US inflation reached a level of 3.0% in June 2023 (after peaking at 9.1% in June 2022). US inflation ended the year at 3.4%.

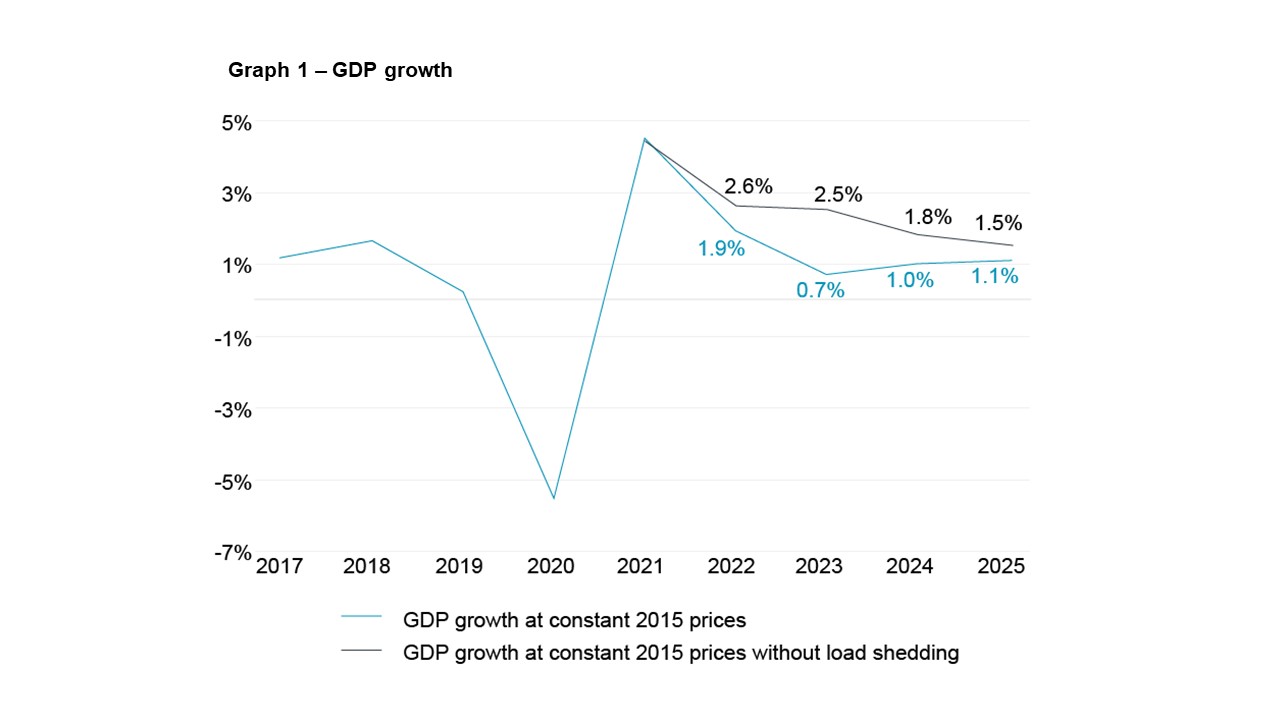

At the outset of 2023, economic growth for South Africa was expected to be approximately 0.1% for the year. As it turns out, and despite record levels of rolling blackouts, economic growth for the full year is expected to be closer to 0.7%.

Although better than anticipated, economic growth of 0.7% p.a. for South Africa remains disappointing. The low growth path is a direct result of the ongoing electricity shortage experienced in South Africa. According to the South African Reserve Bank, South Africa’s economic growth could have been as high as 2.5% in 2023 had it not been for the load shedding experienced in 2023 (graph 1).

{kind=link}

Lower inflation prevailed in South Africa in 2023. After peaking at 7.8% in July 2022, the inflation rate reached a low of 4.7% in July 2023. Towards year-end, inflation rebounded to 5.9%.

The Monetary Policy Committee of the South African Reserve Bank continued with its hawkish policy by increasing its repurchase rate by 0.25% early in January 2023 and again by 0.50% in May 2023.

Employment numbers in South Africa improved in 2023. By September 2023, employment had grown by 811 000 jobs for the nine months. The number of jobs added for the full year could exceed one million jobs. The official unemployment rate was at 31.9% compared to 32.7% in 2022. Employment also improved when measured using the expanded definition (which includes discouraged job seekers), to 39.7% in September 2023 from 40.9% in 2022. While the improvement is encouraging, the progress made with employment is insufficient to satisfy the requirements of a growing population.

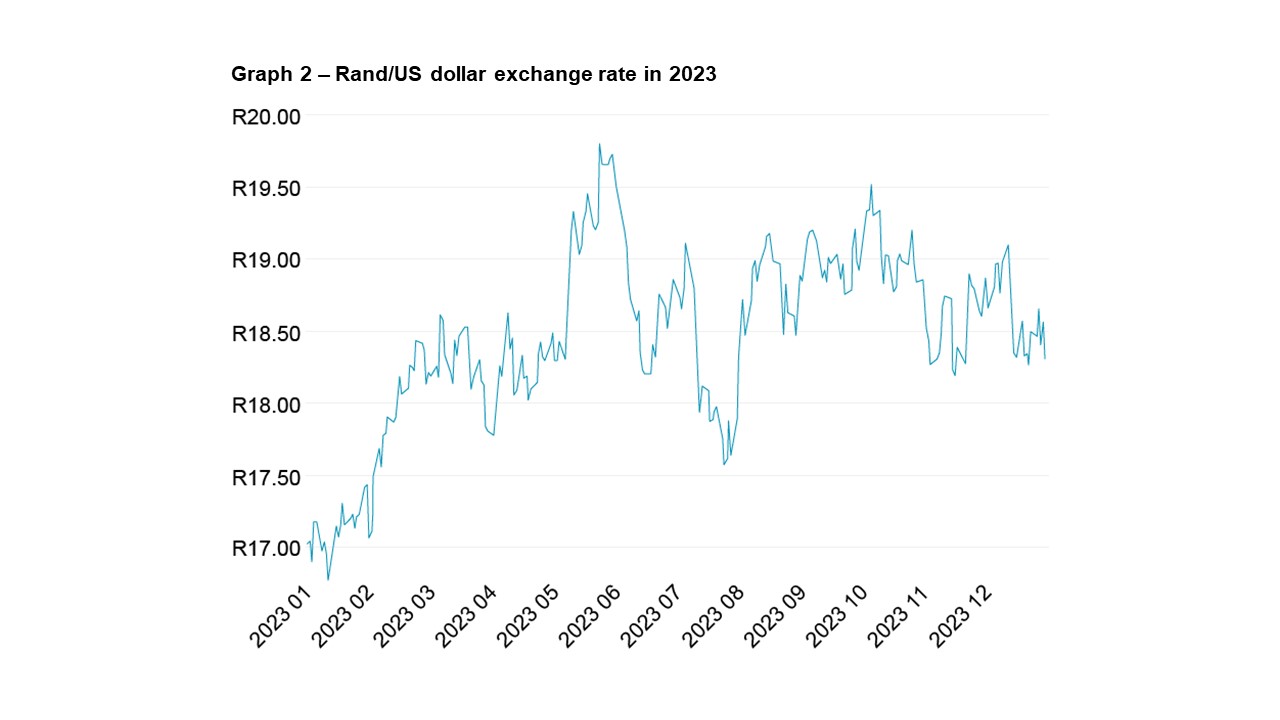

The exchange rate of the rand was volatile in 2023 (graph 2). The rand opened at R17.00 in 2023 and closed the year at R18.30, but on average, the daily closing value of the rand was R18.45 in 2023. During the year the rand traded as strongly as R16.60 (in January 2023) and as weakly as R20.01 (in May 2023).

Graph 2 – Rand/US dollar exchange rate in 2023

{kind=link}

In 2023, the price of oil traded as low as US$71.84 (June 2023) before increasing to $96.55 (September 2023). It closed the year at $77.04. Combined with changes in the exchange rate of the rand, the changes to the oil price saw the price of petrol in South Africa (inland, highest octane) drop to R22.46 in July 2023 but it rose to R25.68 in October 2023. . At the beginning of 2024, the price of petrol was back down to R22.49 per litre.

Geopolitical uncertainty prevailed around the world as the Russian-Ukrainian war continued and renewed conflict between Israel and the Palestinian movement Hamas flared up in October 2023.

Financial markets

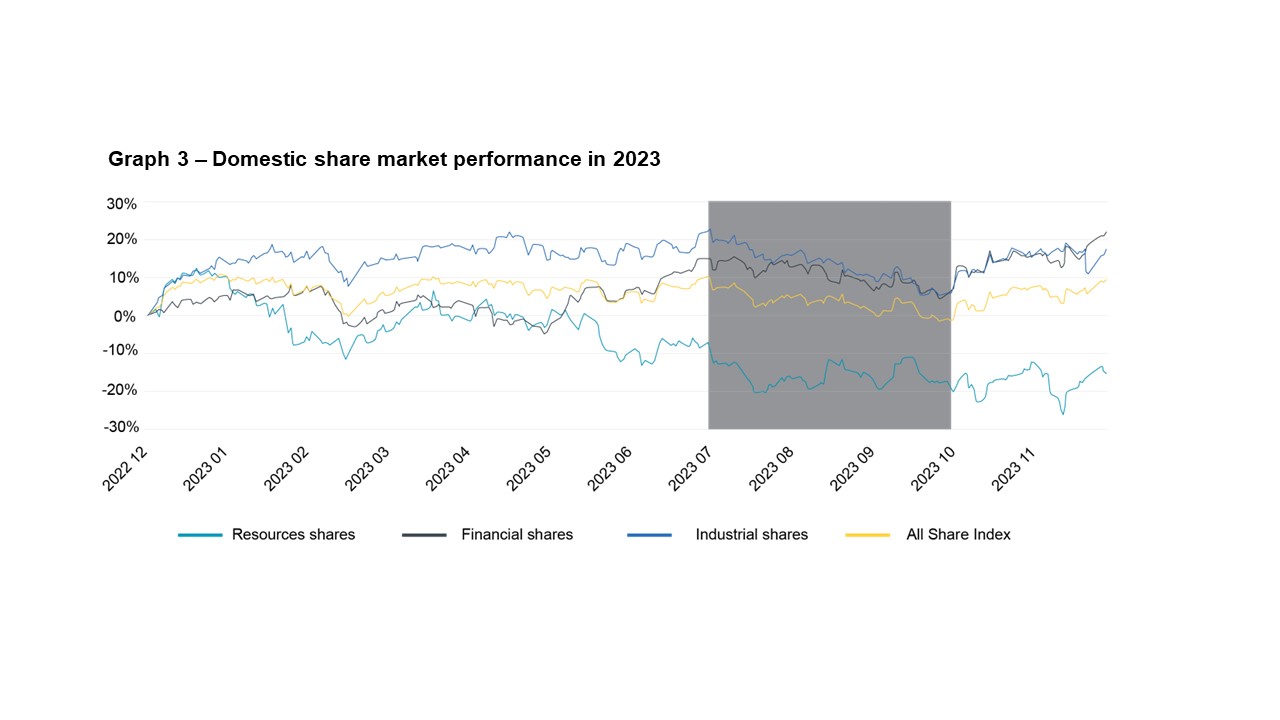

After experiencing pressure in Q3 of 2023, financial market conditions improved in November and December 2023. The FTSE/JSE All Share Index TR improved by 10.7% over the last two months of 2023 achieving 9.3% for the full year. The improved investment returns were spearheaded by financial shares (up 14.7%). Industrial shares were up 11.0% and even resources shares improved by 4.5% during November and December 2023. For 2023, financial shares gained 21.8% and industrial shares rose 17.3%, but resources shares lost 15.4%. The shaded area in graph 3 shows the period when the prices of financial assets came under pressure.

Graph 3 – Domestic share market performance in 2023

{kind=link}

Listed property performed particularly well during the recovery phase in November and December 2023 (up 20.0%) and the 12-month return also showed some recovery (up 10.1%) following the dismal returns generated since 2017.

The FTSE/JSE All Bond Index achieved a return of 9.7% in 2023 (of which 6.6% came in November and December 2023). Bonds in the 7 to 12 years category performed best by achieving a return of 11.9% in 2023 (7.5% in November and December 2023). For the full year, long bonds in the 12 years+ category generated modest returns of 7.5% only. In the money market, the STeFI Composite Index closed the year up 8%.

Offshore shares contributed significantly to investment returns in 2023 by generating a rand return of 32.3% for the year (12.7% in November and December 2023). Offshore shares’ return in local currency (23.1%) was boosted by rand weakness of 7.0% in 2023. Offshore bonds closed the year 13.6% better in rand terms (5.7% in local currency).

Non-resident investors continued to sell their exposure to South African bonds and shares. The JSE reported share sales by non-resident investors of R193 billion in 2023, and based on information released by National Treasury we estimate that non-residents reduced their South African bond exposure by at least R14 billion in 2023.

The investment returns generated by the indices representing the asset classes in which South African retirement funds typically invest are shown in the table below:

| % Change December 2023 | Most recent quarter | Calendar

YTD |

1 year

(p.a.) |

3 years (p.a.) | 5 years (p.a.) | 10 years (p.a.) |

| All Share Index | 6.9% | 9.3% | 9.3% | 15.4% | 15.1% | 8.8% |

| Listed Property | 16.4% | 10.1% | 10.1% | 17.2% | 0.2% | 2.9% |

| STeFI Composite | 2.1% | 8.0% | 8.0% | 6.0% | 6.7% | 6.4% |

| ALBI | 8.1% | 9.7% | 9.7% | 8.0% | 9.7% | 8.0% |

| MSCI All Country World ZAR | 7.7% | 32.3% | 32.3% | 14.4% | 17.9% | 14.9% |

| Bloomberg Global Aggr. Bond ZAR | 4.5% | 13.6% | 13.6% | 1.6% | 4.6% | 6.3% |

| Rand (+ stronger, – weaker) | 3.4% | -7.0% | -7.0% | -6.6% | -4.3% | -4.3% |

| Inflation (estimate) | 0.8% | 5.1% | 5.1% | 6.4% | 5.6% | 6.6% |

| Gold ZAR | 7.9% | 21.6% | 21.6% | 10.7% | 15.5% | 11.7% |

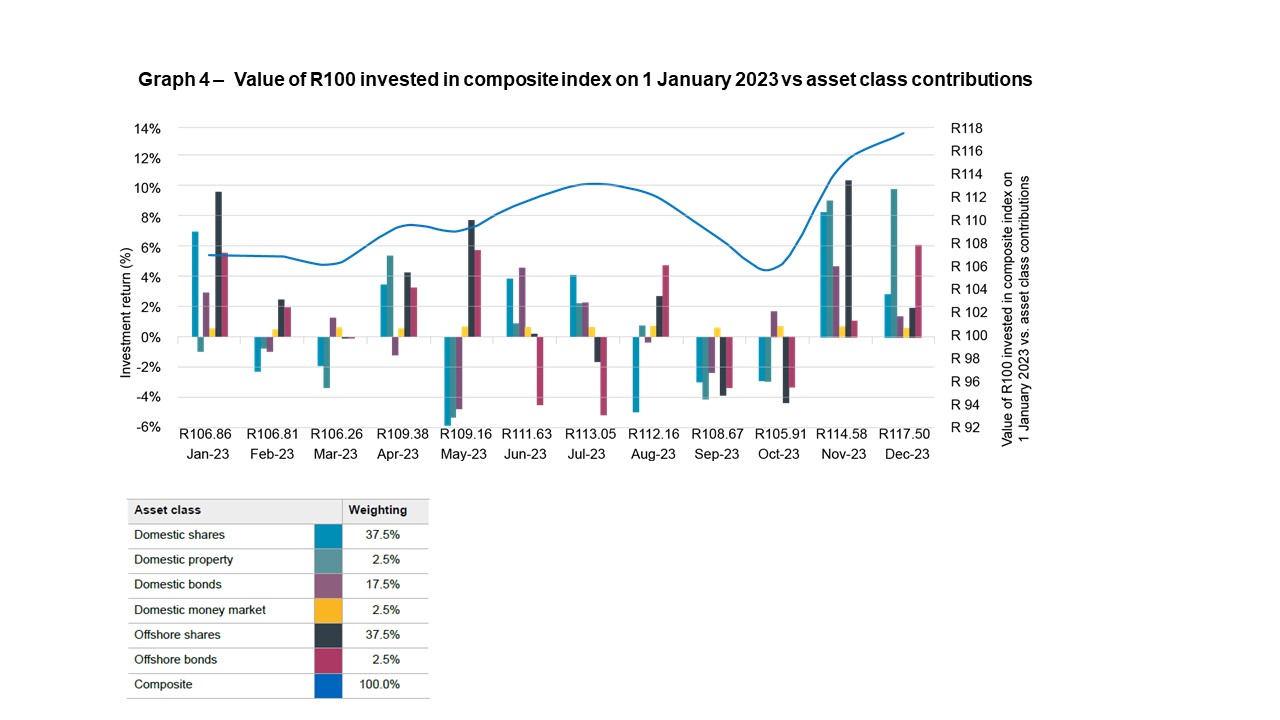

The investment return on an aggressive Regulation 28 compliant index composite with high offshore exposure and maximum exposure to shares slowed to approximately 5.9% year to date by October 2023, but as a result of positive market conditions that prevailed in November and December 2023, the expected return for the full calendar year 2023 is 17.5% (graph 4). It must be reiterated that the aggressive benchmark represents a stretch target for fund managers and it would be pleasing for fund managers to reach this target.

Graph 4 – Value of R100 invested in composite index on 1 January 2023 vs asset class contributions

{kind=link}

The 11% return added to the aggressive index composite in November and December 2023 contributed to improved longer-term returns, as the 3-year and 5-year investment returns for the composite now exceed the required return of 5.5% above inflation after fees.

Information for this article has been obtained from several sources: National Treasury, South African Reserve Bank, Stats SA and IRESS