Economic Commentary – Review of Q1/2023

The Economy

Inflation, interest rate increases and slower growth projections for South Africa are dominating the course of economic events as 2023 unfolds. Similar trends are seen elsewhere in the world.

Globally, the banking sector came under pressure as some regional banks in the US such as Silicon Valley Bank and Signature Bank failed, and other banks faced difficulty. The US government stepped in to deploy emergency measures to shore up the banking system and guarantee deposits at two banks that failed. All deposit accounts at both institutions were guaranteed, according to a joint statement released by the US Federal Reserve, the Department of the Treasury and Federal Deposit Insurance Corporation (FDIC). In Switzerland, the distressed Credit Suisse was bought by UBS Group AG for CHF3 billion (US$3.2 billion) in a deal brokered and supported by the Swiss government and the Swiss Financial Market Supervisory Authority. Credit Suisse has been in distress for a number of years and the decision to write down CHF16 billion (US$17.5 billion) of Credit Suisse bonds, known as Additional Tier 1 or AT1 debt, to zero was a condition to the forced rescue merger with UBS.

In South Africa, it is widely anticipated that the economy will expand by only some 0.3% in 2023. (The IMF recently downgraded South Africa’s growth expectation for 2023 by 1.1% to 0.1%, the largest reduction across the globe.) By comparison, the economy expanded by 2.0% for the full year in 2022, despite contracting in the fourth quarter (-1.3%). The slower growth expectations have arisen from a slowing commodity cycle and a regime of higher interest rates to combat inflation. The banking sector reports that households are under pressure, as a rising number of unsecured loans (credit cards) and even secured loans (motor vehicle financing and even housing bonds) are falling in arrears.

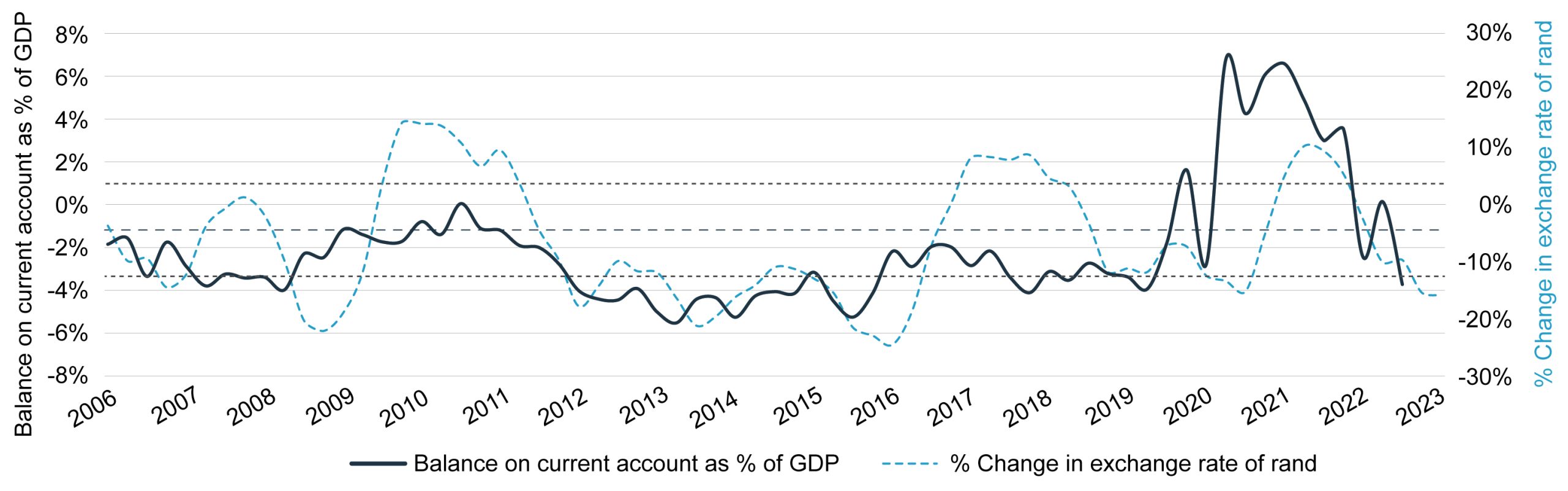

The South African Reserve Bank has raised the repurchase rate twice in Q1 of 2023, by 0.25% in January and, surprisingly, by 0.50% in March 2023. The repurchase rate was 7.75% at quarter-end. To date, the repurchase rate has been raised nine times and by a total of 4.25% since November 2021. The higher-than-anticipated increase in March 2023 points to concerns about inflation, possibly the rand exchange rate and the local current account balance that is swinging into deficit again.

Click here to view graph: Balance on current account as % of GDP vs. % change in exchange rate of rand

{kind=link}

High inflation in Q1 of 2023 was driven by the petrol price, food prices (e.g. bread and chicken), the shortage of electricity, and salary increases. Industry is spending billions of rand on diesel for generators, to remain operating during periods of load shedding.

During the quarter, the oil price came down from US$85 a barrel to below $75. The reduction was welcomed, as it contributed to expectations of a lower petrol price and lower inflation in South Africa. China, Russia and Saudi Arabia engaged in rapprochement and soon afterwards OPEC+ announced oil production cutbacks, with the price of oil overnight jumping back to US$85 a barrel. An oil price at that level is not positive for South Africa’s inflation expectations.

The gold price has improved since 2022 and closed Q1 of 2023 at US$1 975 an ounce. In rand terms, the gold price (e.g. Krugerrands) increased by R6 925 an ounce for the 12 months to March 2023 (24.5%), translating into a rise of US$290.

In his State of the Nation Address to Parliament on 9 February 2023, President Ramaphosa declared a national state of disaster to deal with South Africa’s electricity crisis and announced that a Minister of Electricity would be appointed to address load shedding and related issues. The President delayed the appointment of Mr Kgosientsho Ramokgopa as Minister of Electricity to 6 March 2023. On 6 April 2023, Government announced that the national state of disaster was revoked.

In the meantime, the Minister of Finance presented the National Budget to Parliament on 22 February 2023. The Budget balanced the interests of the needy with the interests of taxpayers. Crucially, it provided for salary increases for government employees of 3% for 2023-24. On 6 March 2023, trade union NEHAWU initiated a strike that turned violent and by 15 March 2023, Government agreed to a salary increase of 7.5% for NEHAWU members. The offer of 7.5% has subsequently been rolled out to all government employees. The irony is that the 7.5% increase was agreed to less than 22 days after the Budget was presented to Parliament and before the Division of Revenue Bill has even been considered by Parliament. The general salary increase of 7.5% for government employees, as opposed to the budgeted 3%, adds approximately R35 billion to government expenses.

South African consumer price inflation was 7.1 % and US consumer inflation was 5.0% for March 2023.

Data released in Q1 of 2023 revealed that employment statistics improved in the period to December 2022. The latest unemployment number is 32.7%, down from 35.3% in the previous year. By December 2022, there were 1 390 000 more people in jobs than the previous year, and using the wider definition of unemployment, 621 000 fewer people were unemployed.

Financial markets

The rand exchange rate weakened by 172c to R18.72 by the Ides of March 2023. By quarter-end, the rand closed at R17.79.

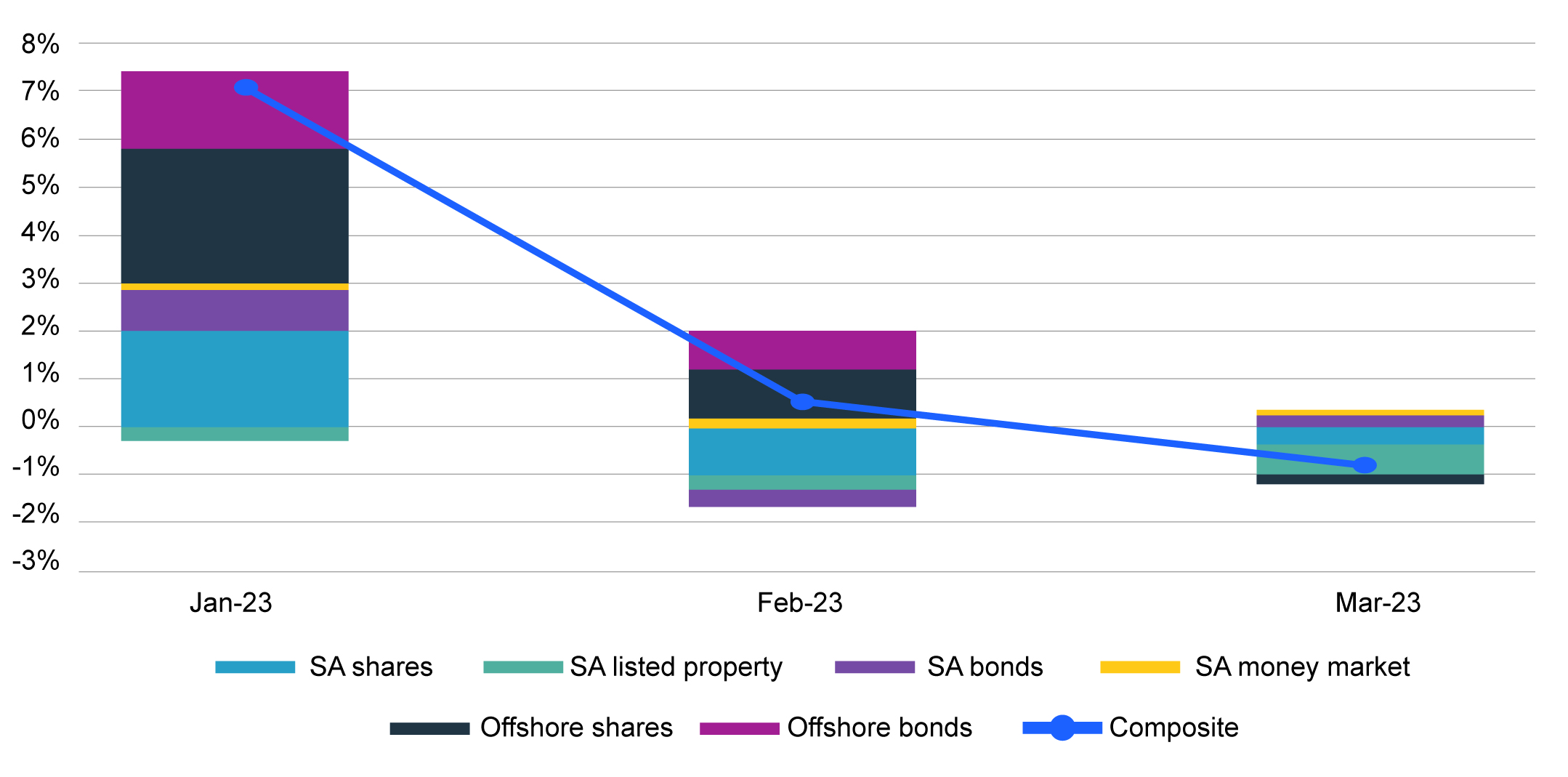

Click here to view graph: Asset class investment returns for Q1 of 2023

{kind=link}

The investment return on a Regulation 28 compliant super-aggressive index composite with maximum offshore exposure and exposure to shares came to 6.7% for Q1 of 2023. Early indications are that global balanced funds achieved returns of about 5% for the quarter.

Rising share prices pushed up investment returns in January 2023. The FTSE/JSE All Share Index jumped 8.9% during January before the rally came to an end in February 2023. However, the index is up only 5.2% for the quarter. The FTSE/JSE All Bond Index added 3.4% and the money market contributed 1.8% whilst listed property lost 5.1% over the 3-month period to March 2023. The weaker rand translated into improved contributions from offshore investment exposure to retirement fund portfolios. Offshore shares generated a rand return of 13.2% for the quarter and offshore bonds added 11.1%.

In the bond market, the best returns were achieved by bonds in the 7- to 12-year bucket for Q1 of 2023 (4.4%), while bonds in the 0- to 3-year bucket delivered the weakest return of 2.6% for the quarter. By quarter-end, the I2029 inflation-linked bond traded at 4.05% and the I2033 inflation-linked bond at 4.55%.

Industrial shares fared the best amongst the three main subsectors over Q1 of 2023 by adding 14.5%, financials traded sideways (0.4%), but resources were down 4.4%. DRD Gold, Gold Fields, AngloGold Ashanti, Aspen Pharmaceuticals and PPC Limited all increased by more than 30% in the quarter. Transaction Capital, Amplats, Thungela Resources, Pick n Pay Stores, Implats, Northam Plats and ArcelorMittal all lost more than 20% over the same period.

The investment returns generated by the indices representing the asset classes in which South African retirement funds typically invest are as follows:

| % Change March 2023 | Most recent quarter | 1 year (p.a.) | 3 years (p.a.) | 5 years (p.a.) |

| All Share Index | 5.2% | 4.9% | 30.5% | 12.8% |

| Listed Property | -5.1% | -3.4% | 21.7% | -3.8% |

| STeFI Composite | 1.8% | 6.0% | 5.1% | 6.5% |

| BEASSA ALBI | 3.4% | 5.8% | 13.0% | 7.9% |

| MSCI All Country World ZAR | 11.1% | 12.1% | 15.4% | 16.4% |

| Barclays Global Aggregate ZAR | 7.6% | 12.0% | -3.5% | 7.1% |

| Rand (+ strengthening, – weakening) | -4.3% | -17.9% | 0.1% | -6.7% |

| Inflation (estimate) | 1.3% | 6.7% | 5.5% | 5.4% |

| Gold ZAR | 13.2% | 24.5% | 6.8% | 17.5% |

Information sourced from: National Treasury, Stats SA and IRESS