ECONOMIC COMMENTARY – JANUARY 2023

Review of Q4 2022

South Africa’s gross domestic product expanded by 1.6% for the third quarter of 2022 (measured quarter on quarter in constant 2015 prices, seasonally adjusted and annualised). Economic output surpassed pre-pandemic levels in the third quarter of 2022. The economy is expected to have achieved real growth of 2.2% year on year for 2022 when the gross domestic product number for the fourth quarter is released on 8 March 2023. The economic sectors that supported expansion included Agriculture, forestry & fishing, Transport, storage & communication, Finance and Construction (off a low base).

The record number of days that South Africa experienced rolling electricity blackouts was a major hindrance to local economic growth in 2022. It seems unlikely that the shortage of electricity will be addressed in the short term.

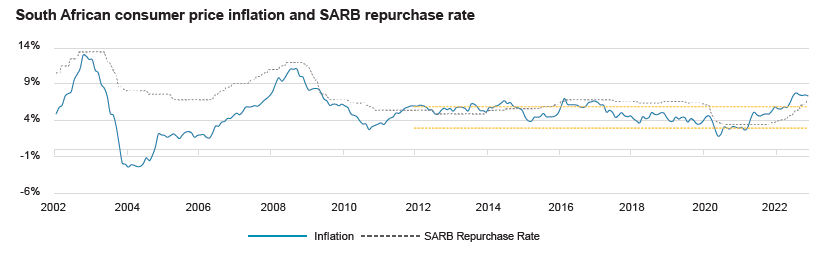

Consumer prices rose 6.8% for the year to November 2022. Consumer price inflation for the full year is likely to be at a similar level. Food prices increased by 12.8% for the year to November 2022, as bread and cereal prices rose 19.9% and the prices of oils and fats soared 24.8%. Prices in expenditure decile 1 (the extremely poor) rose 10.1% for the year to November 2022 and increased by 7.0% for expenditure decile 10 (the highest category). Fuel price inflation for the calendar year to November 2022 is down to 25.3% from the higher levels recorded previously (fuel inflation peaked at 56.2% in July 2022). Inflation is expected to come down, but the elevated level of food price inflation in South Africa still is of concern. Global food price inflation (UN’s FAO Food Price Inflation) for December 2022 is -1.0%.

Graph: South African consumer price inflation and SARB repurchase rate

{kind=link}

The Monetary Policy Committee of the South African Reserve Bank (SARB) continued to increase interest rates in 2022. The repurchase rate was raised six times and by 3.25% in total. Including the interest rate increase late in 2021brings the total increase in the repo rate to 3.5%. Interest rates were increased to combat high inflation and SARB Governor Lesetja Kganyago is reported to have said that inflation is a regressive tax that increases poverty and inequality. Mr Kganyago has communicated that the SARB is prepared to continue raising the repurchase rate until inflation and inflation expectations return to moderate levels (e.g. 4.5%). Most financial market participants expect two further rate hikes of 0.25% each in 2023, with the risk skewed towards three possible rate hikes of 0.25% each.

There were 15.765 million employed people in South Africa as reported in the Quarterly Labour Force Survey for Q3 2022. This is up by 203 000 people from June 2022, but the employment number in South Africa is still 655 000 below pre-pandemic levels. The total unemployed and discouraged job seekers came down by 323 000 from June to September 2022, but there are still 1 658 000 more unemployed and discouraged job seekers compared to pre-pandemic levels. The improvement in employment in 2022 is encouraging, but remains much too modest to be widely noticeable. Jobs were added in the Manufacturing, Trade, catering & accommodation and Transport, storage & communication sectors, but Finance, real estate & business services shed jobs in 2022.

Currency exchange rates were dominated by the strength of the US dollar in 2022. The strengthening US dollar put pressure on the exchange rate of the South African rand. This helped exporting industries (e.g. mining, agriculture and manufacturing) but hurt importing industries (e.g. oil & fuel), which in turn contributed to higher inflation.

The risks posed by geopolitical instability – most notably Russia’s invasion of neighbouring Ukraine and Ukraine’s plucky resistance – affected global economies in 2022. There are those who expected the military action to be short and decisive. This is not the case and Ukraine is fighting back hard. Energy prices, wheat and other agricultural commodity prices rose sharply during the first phases of the war. The oil price subsided from the early elevated levels to a more sustainable level of approximately US$80 a barrel.

The high food and energy prices that prevailed energised voters in democracies around the world to change their governments. In 2022, new administrations took charge in Australia, Brazil, Ireland, Italy, Sweden and the United Kingdom (UK) (twice). The 44-day long premiership of Ms Liz Truss in the UK, based on her ambitious economic stimulation plan, shows that even politicians (in this case the Conservative Party MPs who elected her prime minister) find it difficult to manage an economy facing challenges. Unlike the change of governments in certain countries, the Chinese Communist Party re-elected Xi Jinping as president of the Communist Party and effectively president of the People’s Republic of China. During the US mid-term elections, control of the House of Representatives changed to the Republican Party, but the Democrats kept control of the Senate.

Global financial markets experienced one of their worst periods in recorded history in 2022, as both equities and bonds sold off significantly. Share prices in developed markets fell by about 20% for the year and government bonds in developed markets were down approximately 16%. The US dollar strengthened by 19% to September 2022 but closed the year up only 8%. This was reflected in the exchange rate of the rand, which weakened by 13% against the greenback to October 2022 but closed the year only 6% down against the dollar. The rand kept its value against the cross currencies (e.g. euro, sterling, Australian dollar).

The FTSE/JSE All Share Index followed global share prices down for most of the year (-13% through to October 2022) but recovered strongly in the last quarter to close the year down only 0.9%. Adjusting for dividends, the index achieved a total positive return of 3.6% for the year, adding 15.2% in the last quarter of 2022. Financial shares outperformed resources and industrial shares for the year, but industrial shares recovered especially in the last quarter of 2022 (+17.0%). The Naspers share price rose 98% from May 2022. Listed property also experienced a difficult period with an annual return of 0.5%, achieved only because of the 19.3% posted in the last quarter.

The BEASSA All Bond Index advanced 4.3% for full year, boosted by the 5.3% achieved in the last quarter of 2022.

| % Change December 2022 | Most recent quarter | 1 year (p.a.) | 3 years (p.a.) | 5 years (p.a.) |

| All Share Index | 15.2% | 3.6% | 14.4% | 9.4% |

| Listed Property | 19.3% | 0.5% | -3.3% | -6.3% |

| STeFI Composite | 1.6% | 5.2% | 5.0% | 6.5% |

| BEASSA ALBI | 5.7% | 4.3% | 7.6% | 9.2% |

| MSCI All Country World ZAR | 3.4% | -12.4% | 11.5% | 12.7% |

| Barclays Global Aggregate ZAR | -1.6% | -10.4% | 2.0% | 4.8% |

| Rand (+ strengthening, – weakening) | 6.3% | -6.4% | -5.9% | -5.5% |

| Inflation (estimate) | 0.9% | 7.1% | 5.6% | 5.4% |

| Gold ZAR | 3.4% | 6.5% | 13.3% | 14.1% |

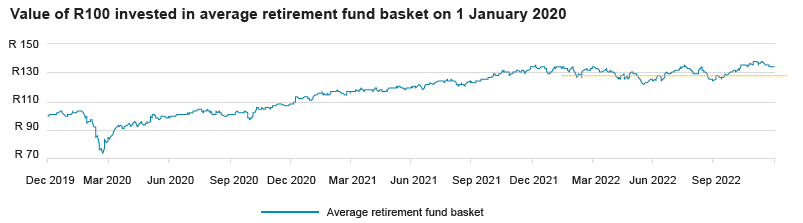

The question asked by those who save for retirement is how the volatility in financial markets affected their retirement savings.

Despite the very difficult conditions that prevailed in financial markets over the last three years, R100 invested in an average retirement fund balanced growth portfolio on 1 January 2020 would have grown to R134.44 by 31 December 2022. This represents a compound annualised growth rate of 10.4%.

Graph -Value of R100 invested in average retirement fund basket on 1 January 2020

{kind=link}

The long-term investment return required for retirement funds is 6.0% above inflation and after fees. Long-term inflation is expected to be 6.0% (the average inflation rate since 1994 is 6.0%). Using a fee of 0.75% p.a., the required nominal investment return for a retirement savings portfolio is 12.75% p.a. This means over the last three years there has been a shortfall, as the average retirement fund portfolio achieved only 10.4% p.a.

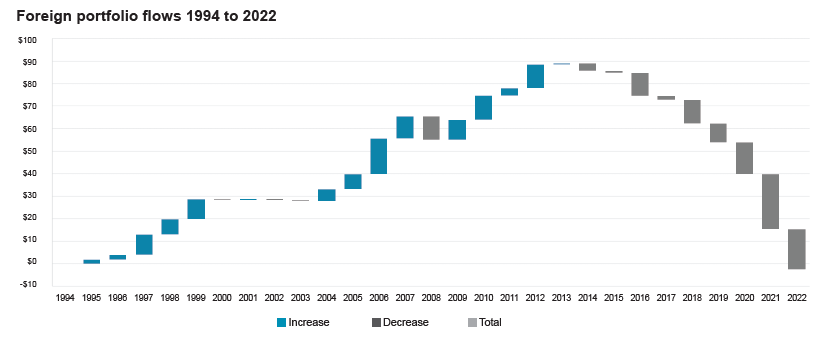

Interestingly, South Africa’s financial markets are now net exporters of capital (in US dollars) since 1994. The cumulative value reported by the JSE settlement system shows that the US$2.342 billion worth of investments sold off by foreign investors in December 2022 resulted in the JSE becoming an exporter of capital.

Graph 3 – Foreign portfolio flows 1994 to 2022

{kind=link}

This trend could very well be reversed in 2023.

The likelihood of an economic recession in developed economies in 2023 is significant and follows on a regime of maintaining high interest rates to combat inflation. Elevated interest rate levels eventually lead to demand for goods and services contracting and inflation subsiding.

Will an economic recession lead to another bear market (e.g. investment returns of -10% p.a.) or a repeat of 2022 in financial markets, when global share and bonds prices fell by 20% and 15% respectively?

A bear market or repeat of 2022 is unlikely, as financial markets are forward looking and discount future growth and economic developments. The economic recessions that are widely predicted for 2023 have already played havoc in financial markets in 2022. Financial markets are more likely to be driven by expectations of future developments, i.e. economic conditions in 2024 and onwards. Unless the news flow that informs expectations for economic conditions from 2024 provides negative surprises, we expect a recovery in investment markets during 2023. However, investment markets are expected to remain volatile during the year.

Information sourced from: Stats SA, SARB, UN Food and Agriculture Organisation, Iress and BizNews