An update on our investment outlook for 2023 – 6 April 2023

An update on our investment outlook for 2023

We are three months into 2023, and it may be helpful to review the market outlook we released as Investment Notes 1/2023 – Where will financial markets take investors in 2023?

This was our premise at the start of the year:

- Inflation is likely to trickle down, leading to lower bond yields and pleasing equity market performance.

- Bonds would be the top performing asset class in 2023, followed by equities, then listed property, with money market instruments providing a fair return.

- The US dollar was expected to weaken, which would have resulted in a stronger rand/dollar exchange rate.

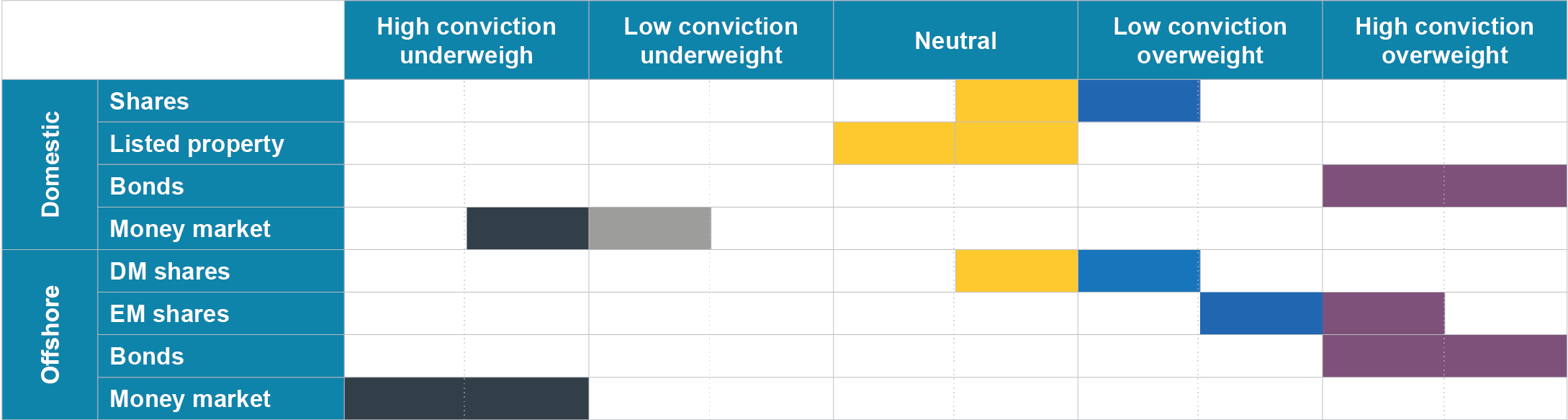

Click here to view our outlook for fund positioning at the outset of the year.

{kind=link}

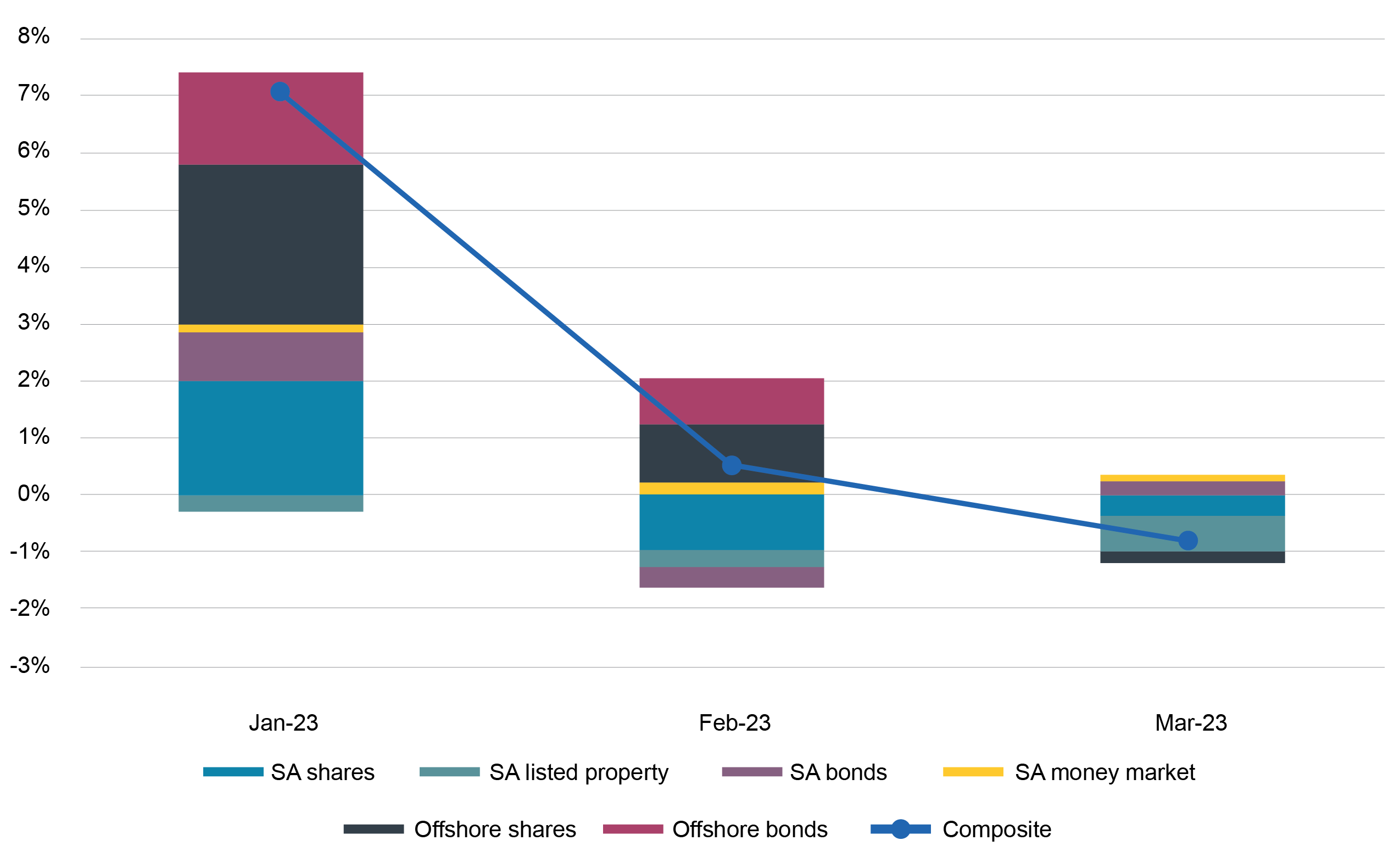

As it happened, the year started with a strong rally in equity markets – which, if it continued, would have made a mockery of our somewhat cautious outlook. The US dollar exchange rate weakened as expected, but unexpectedly, the rand exchange rate weakened as well. The FTSE/JSE TOPI40 Index was up 9.7% for the month of January 2023 and on average, global balanced funds were up 6.0% over the same period.

The index-based investment return for a typical Regulation 28-compliant composite fund is shown below.

By the end of March 2023, investment returns were more sobering than the heady levels achieved in January 2023. The FTSE/JSE TOPI40 Index is up 5.2% for the quarter and down 4.2% from January 2023. The average return for global balanced funds is expected to be approximately 5.8% to 6.0% for the quarter to March 2023 (fund returns are usually slightly lower than the index-based composite return, which is more aggressive and maintains maximum exposure to shares and offshore investments and excludes transaction costs and in-fund fees).

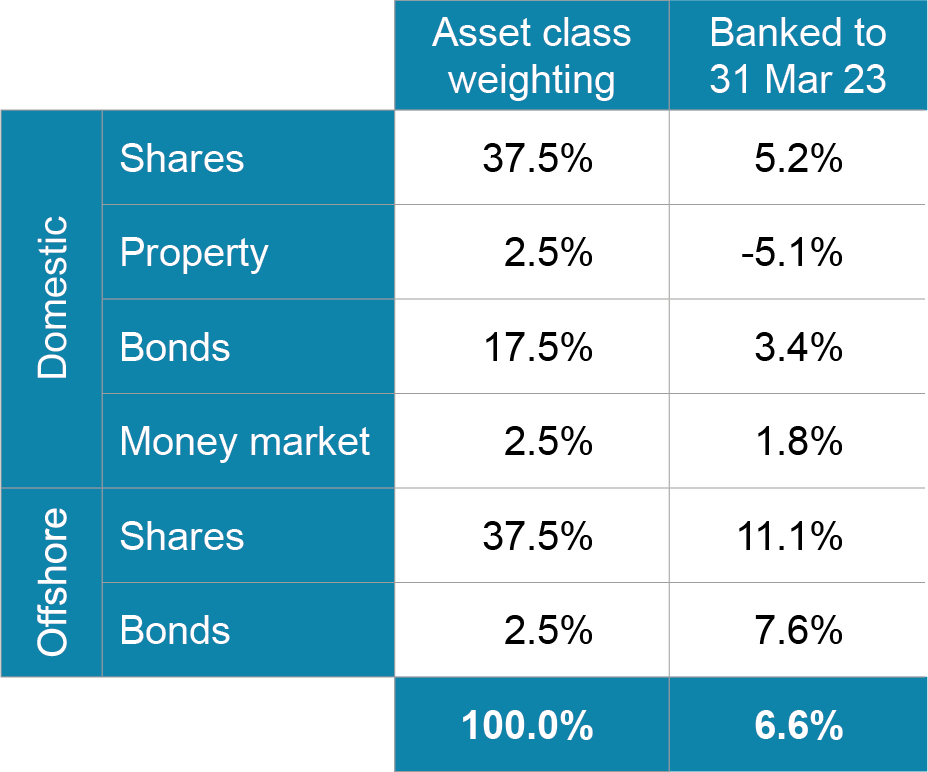

Return for Regulation 28-compliant composite

| Asset class weighting | Banked to 31 Mar 23 | ||

| Domestic | Shares | 37.5% | 5.2% |

| Property | 2.5% | -5.1% | |

| Bonds | 17.5% | 3.4% | |

| Money market | 2.5% | 1.8% | |

| Offshore | Shares | 37.5% | 11.1% |

| Bonds | 2.5% | 7.6% | |

| 100.0% | 6.6% |

Graph: Return for Regulation 28-compliant composite

{kind=link}

With a return of approximately 5.8% in the bank to March 2023, how will the remainder of the year play out?

Our conviction is that four factors will be crucial going forward. As articulated in January 2023, we believe that lower inflation and lower bond yields will set the direction for the remainder of 2023. The third factor is South Africa’s fiscal position, which, after Government agreeing to a 7.5% wage increase for government employees, may raise challenges not foreseen by the Minister of Finance or National Treasury in the 2023/24 National Budget. If general wages increase by 7.5%, the actual increase to the wage account may be even higher. The fourth factor is the (global) sentiment that prevails in financial markets.

Inflation is dropping at a much more perambulating pace than expected originally. Central banks have indicated their willingness to increase policy interest rates by as much as is needed to bring inflation into line. Inflation is an additional tax faced by salary and wage earners, so the commitment of central banks to combat inflation should be applauded. The question is to which extent inflation is currently driven by demand-side factors as opposed to supply-side constraints. Hiking interest rates is usually effective when addressing demand-side inflation, but less so when tackling inflation created by supply-side constraints. Raising interest rates to reduce inflation driven by supply-side constraints could do further damage to the banking sector and harm economic prospects. We have already seen established banks being severely disrupted by the pace of the increase in interest rates over the last year or so. This provides central banks with an additional consideration in managing inflation. Lower inflation and lower bond yields are essential ingredients to economic recovery in the months to come and to positive results in equity markets.

The general increase in the wages of government employees of 7.5% instead of the 2.5% provided for by National Treasury in the 2023/24 Budget increases expenditure by R32.5 billion. This is equal to 1.6% of total revenue and will increase the national deficit from the Minister’s projection of 4.2% to 5.8% in 2023-24. As National Treasury will be providing R254 billion debt relief to Eskom already, the further R32.5 billion is but another straw added to the camel’s back. More loans will have to be raised in the capital markets.

Global sentiment in financial markets is currently hesitant but may well improve as the year continues. What is clear though, is that global investors continue to sell off South African exposure. Net sales of South African shares by foreign residents amount to R57 billion from January to March 2023 and net sales of South African bonds recorded by the JSE settlement system amount to R82 billion from January to March 2023. The combined net sales from January to March 2023 are R140 billion (compared to R102 billion for the same period in 2020 during the Covid crash, R62 billion in 2021 and R26 billion in 2022).

How does this change our outlook for 2023?

{kind=link}

We maintain our cautiously optimistic outlook for domestic shares, but our expectation of offshore shares has improved somewhat because of the weaker rand exchange rate and the strong contribution over the period from January to March 2023. We do realise that share prices in some developed markets are considered to be expensive. We have also adopted a slightly more careful stance on domestic and offshore bond returns because inflation remains higher than we initially expected in 2023.

A significant change to our position from January 2023, is that our analysis shows the contributions made by domestic and offshore shares to balanced growth funds are expected to be similar in 2023, which creates the opportunity for balanced funds to fully use their offshore allowance in 2023.

We still expect double-digit investments returns for 2023.

Information for this article obtained from several sources: National Treasury Budget 2023-24 and IRESS.